Udemy - PHP Symfony 4 API Platform + React.Js Full Stack Masterclass

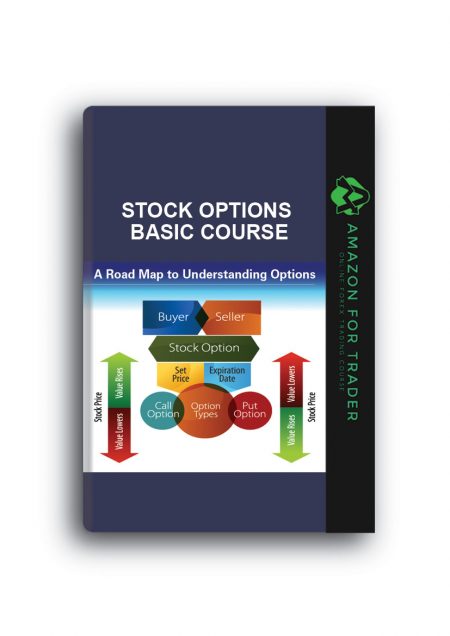

Udemy - PHP Symfony 4 API Platform + React.Js Full Stack Masterclass STOCK OPTIONS BASICS COURSE - Follow Me Trades

STOCK OPTIONS BASICS COURSE - Follow Me Trades FOLLOWMETRADES – MASTER TRADER COURSE

FOLLOWMETRADES – MASTER TRADER COURSE OPTIONPIT – MAXIMIZING PROFITS WITH WEEKLY OPTIONS TRADING

OPTIONPIT – MAXIMIZING PROFITS WITH WEEKLY OPTIONS TRADING

Description

Keith Allman – Reverse Engineering Deals on Wall Street with Microsoft Excel

Description

A serious source of information for those looking to reverse engineer business deals

It’s clear from the current turbulence on Wall Street that the inner workings of its most complex transactions are poorly understood. Wall Street deals parse risk using intricate legal terminology that is difficult to translate into an analytical model. Reverse Engineering Deals on Wall Street: A Step-By-Step Guide takes readers through a detailed methodology of deconstructing the public deal documentation of a modern Wall Street transaction and applying the deconstructed elements to create a fully dynamic model that can be used for risk and investment analysis.

Appropriate for the current market climate, an actual residential mortgage backed security (RMBS) transaction is taken from prospectus to model by the end of the book. Step by step, Allman walks the reader through the reversing process with textual excerpts from the prospectus and discussions on how it directly transfers to a model. Each chapter begins with a discussion of concepts with exact references to an example prospectus, followed by a section called “Model Builder,” in which Allman translates the theory into a fully functioning model for the example deal. Also included is valuable VBA code and detailed explanation that shows proper valuation methods including loan level amortization and full trigger modeling.

Aside from investment analysis this text can help anyone who wants to keep track of the competition, learn from others public transactions, or set up a system to audit one’s own models.

Note: CD-ROM/DVD and other supplementary materials are not included as part of eBook file.

Table of Contents

Preface.

Acknowledgments.

About the Author.

CHAPTER 1: Introduction.

The Transaction.

The Documents.

The Process.

How This Book Works.

CHAPTER 2: Determining Dates and Setting Up Timing.

Differences in Timing Approaches.

A First Look at the Prospectus.

Important Dates.

Transforming Dates and Timing from Words to a Model.

Model Builder 2.1: Reversing Dates and Timing.

Conclusion of Dates and Timing.

CHAPTER 3: Creating Asset Cash Flow from Prospectus Data.

It’s All in the Prospectus Supplement.

The Basics of Amortization.

Performance and the Prospectus Supplement.

Delinquency.

Loss.

Prepayment.

Recovery.

Creating Cash Flow.

A Complex Implementation.

Model Builder 3.1: Entering in the Raw Asset Information.

Model Builder 3.2: Entering in the Default and Prepayment Assumptions.

Model Builder 3.3: Interest Rates and Additional Asset Amortization Inputs.

Model Builder 3.4: Introducing VBA and Moving Data In and Out of the Model.

Model Builder 3.5: Loading Loan Performance Assumptions into VBA.

Model Builder 3.6: Global Functions.

Model Builder 3.7: Loan-Level Asset Amortization.

CHAPTER 4: Setting Up Liability Assumptions, Paying Fees, and Distributing Interest.

Identifying the Offered Securities.

Model Builder 4.1: Transferring the Liability Information to a Consolidated Sheet.

The Liability Waterfall: A System of Priority.

Model Builder 4.2: Starting the Waterfall with Fees.

Interest: No Financing Is Free.

Model Builder 4.3: Continuing the Waterfall with Interest Paid to the Certificate Holders.

More on Waterfalls and Wall Street’s Risk Parsing.

Model Builder 4.4: Mezzanine Interest.

Continuing the Waterfall: It Only Gets More Complicated.

CHAPTER 5: Principal Repayment and the Shifting Nature of a Wall Street Deal.

Model Builder 5.1: The Deal State and Senior Principal.

Mezzanine Principal Returns.

Model Builder 5.2: The Mezzanine Certificates’ Priority of Payments.

Number Games or Risk Parsing?

CHAPTER 6: Credit Enhancement Mechanisms to Mitigate Loss.

Model Builder 6.1: Excess Spread, Overcollateralization, and Credit Enhancement.

CHAPTER 7: Auditing the Model.

Model Builder 7.1.

CHAPTER 8: Conclusion of Example Transaction and Final Thoughts on Reverse Engineering.

Mortgage Insurance and Servicer Advances.

Reverse Engineering in the Current and Future Market.

Appendix.

Automatic Range Naming.

About the CD-ROM.

Index.

Author Information

Keith A. Allman is a capital markets professional with a specialization in analytics and modeling. He is currently the principal trainer and founder of Enstruct, a quantitative finance training company, as well as a Managing Director with NSM Capital Management. Prior to this, Allman was a vice president at Citigroup’s Global Corporate and Investment Bank. He has also worked for MBIA Corporation in their Quantitative Analytics division. Allman is the author of Modeling Structured Finance Cash Flows with Microsoft Excel, which is published by Wiley.

Keith Allman, Reverse Engineering Deals on Wall Street with Microsoft Excel, Download Reverse Engineering Deals on Wall Street with Microsoft Excel, Free Reverse Engineering Deals on Wall Street with Microsoft Excel, Reverse Engineering Deals on Wall Street with Microsoft Excel Torrent, Reverse Engineering Deals on Wall Street with Microsoft Excel Review, Reverse Engineering Deals on Wall Street with Microsoft Excel Groupbuy.

Reviews

There are no reviews yet.