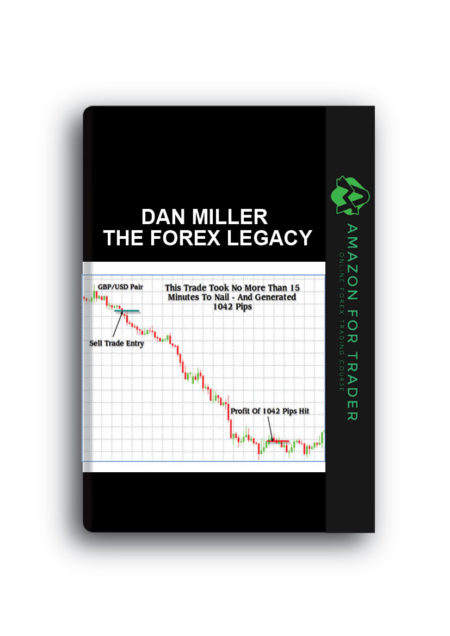

Dan Miller – The Forex Legacy (theforexlegacy.com)

Dan Miller – The Forex Legacy (theforexlegacy.com) Darrell Duffie – Credit Risk

Darrell Duffie – Credit Risk Craig Bttlc – The Adventures of the Cycle Hunter

Craig Bttlc – The Adventures of the Cycle Hunter TRIFORCE TRAINING Part 2

TRIFORCE TRAINING Part 2 Carlos Usabiaga Ibanez – The Current State of Macroeconomics

Carlos Usabiaga Ibanez – The Current State of Macroeconomics Alpesh Patel Package ( Discount 20% )

Alpesh Patel Package ( Discount 20% ) Donald D.Hester – The Evolution of Monetary Policy & Banking in the US

Donald D.Hester – The Evolution of Monetary Policy & Banking in the US Aspatore Books – Inside the Minds Leading Wall Street Investors

Aspatore Books – Inside the Minds Leading Wall Street Investors CashFlow Heaven – Trade from Anywhere (tradefromanywhere.com)

CashFlow Heaven – Trade from Anywhere (tradefromanywhere.com) J.Franke, W. Hardle, G. Stahl – Measuring Risk in Complex Stochastic Systems

J.Franke, W. Hardle, G. Stahl – Measuring Risk in Complex Stochastic Systems Carlos M.Pelaez – The Global Recession Risk

Carlos M.Pelaez – The Global Recession Risk

Description

J.Franke, W. Hardle, G. Stahl – Measuring Risk in Complex Stochastic Systems

Since the seminal of Markowitz (1952) and Sharpe (1964) capital allocation within portfolios is based on the variance/covariance analysis. Even the introduction of Value-at-Risk in order to measure risk more accurately than in terms of standard deviation, did not chance the calculation of a risk contribution of single asset in the portfolio or its contributory capital as a multiple of the asset’s β with the portfolio. This approach is based on the assumption that asset returns are normally distributed. Under this assumption, the capital of a portfolio, usually defined as a quantile of the distribution of changes of the portfolio. Since the βs yield a nice decomposition of the portfolio standard deviation and exhibit the interpretation as an infinitesimal marginal risk contribution (or more mathematically as a partial derivative of the portfolio standard deviation with respect to an increase of the weight of an asset in the portfolio), these useful properties also hold for the quantie, i.e. for the capital.

J.Franke, W. Hardle, G. Stahl, Measuring Risk in Complex Stochastic Systems, Download W. Hardle, Free W. Hardle, W. Hardle Torrent, W. Hardle Review, W. Hardle Groupbuy, Download G. Stahl, Free G. Stahl, G. Stahl Torrent, G. Stahl Review, G. Stahl Groupbuy, Download Measuring Risk in Complex Stochastic Systems, Free Measuring Risk in Complex Stochastic Systems, Measuring Risk in Complex Stochastic Systems Torrent, Measuring Risk in Complex Stochastic Systems Review, Measuring Risk in Complex Stochastic Systems Groupbuy.

Reviews

There are no reviews yet.