Sankar Pal – Mathematical Programming and Game Theory for Decision Making

Sankar Pal – Mathematical Programming and Game Theory for Decision Making Trading Double Diagonals in 2019 - Sheridan Mentoring

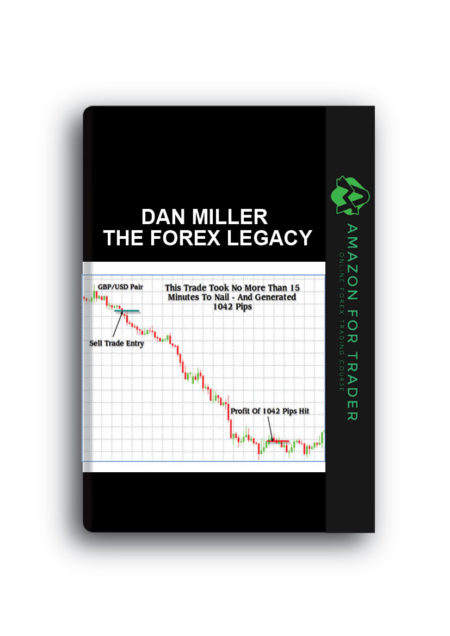

Trading Double Diagonals in 2019 - Sheridan Mentoring Dan Miller – The Forex Legacy (theforexlegacy.com)

Dan Miller – The Forex Legacy (theforexlegacy.com) Adrienne Laris Toghraie – Traders Business Plan

Adrienne Laris Toghraie – Traders Business Plan Terry Townsend – Cotton Trading Manual

Terry Townsend – Cotton Trading Manual Larry Connors - Advanced Trading Strategies

Larry Connors - Advanced Trading Strategies Gilbert W.Fairholm - Mastering Inner Leadership

Gilbert W.Fairholm - Mastering Inner Leadership TRIFORCE TRAINING Part 2

TRIFORCE TRAINING Part 2 Trading Double Calendar in 2018 - Sheridan Options Mentoring

Trading Double Calendar in 2018 - Sheridan Options Mentoring John Bollinger – Bollinger on Bollinger Bands (Video 2.54 GB)

John Bollinger – Bollinger on Bollinger Bands (Video 2.54 GB) Carlos Usabiaga Ibanez – The Current State of Macroeconomics

Carlos Usabiaga Ibanez – The Current State of Macroeconomics Carlos M.Pelaez – The Global Recession Risk

Carlos M.Pelaez – The Global Recession Risk John O.Rawlings – Applied Regression Analysis

John O.Rawlings – Applied Regression Analysis ERIC WORRE – RADICAL DUPLICATION

ERIC WORRE – RADICAL DUPLICATION Aspatore Books – Inside the Minds Leading Wall Street Investors

Aspatore Books – Inside the Minds Leading Wall Street Investors")

Description

Andrew W.Lo – Long-Term Memory in the Stock Market Prices (Article)

A test for long-run memory that is robust to short-range dependence is developed. It is a simple extension of Mandelbrot’s “range over standard deviation” or R/S statistic, for which the relevant asymptotic sampling theory is derived via functional central limit theory. This test is applied to daily, weekly, monthly, and annual stock returns indexes over several different time periods. Contrary to previous findings, there is no evidence of long-range dependence in any of the indexes over any sample period or sub-period once short-term autocorrelations are taken into account. Illustrative Monte Carlo experiments indicate that the modified R/S test has power against at least two specific models of long-run memory, suggesting that stochastic models of short-range dependence may adequately capture the time series behavior of stock returns.

Andrew W.Lo, Long, Term Memory in the Stock Market Prices (Article), Download Long, Free Long, Long Torrent, Long Review, Long Groupbuy, Download Term Memory in the Stock Market Prices (Article), Free Term Memory in the Stock Market Prices (Article), Term Memory in the Stock Market Prices (Article) Torrent, Term Memory in the Stock Market Prices (Article) Review, Term Memory in the Stock Market Prices (Article) Groupbuy.

Reviews

There are no reviews yet.